Short Squeeze Fundamentals

What Is Short Interest?

Short interest is the percentage of a stock’s float that has been sold short by traders and hasn’t been covered yet. It represents the cumulative bearish bets against the stock from all market participants. The formula is: Short Interest % = (Shares Sold Short / Float) × 100.

For example, if a stock has a float of 50 million shares and 12 million shares have been sold short, the short interest calculates to (12M / 50M) × 100 = 24%. This means nearly 1 in 4 shares are currently sold short, and those short sellers are waiting for the price to drop so they can buy back cheaper.

Short interest percentages convey different levels of market sentiment and squeeze potential:

- Below 5%: Low, normal short activity with essentially no squeeze potential

- 5-10%: Moderate short interest where some traders are bearish but not enough to create meaningful squeeze risk

- 10-20%: Elevated short interest indicating strong bearish sentiment and growing squeeze potential

- 20-30%: Very high short interest with significant squeeze potential due to trapped shorts

- Above 30%: Extreme short interest with very high squeeze risk if price reverses

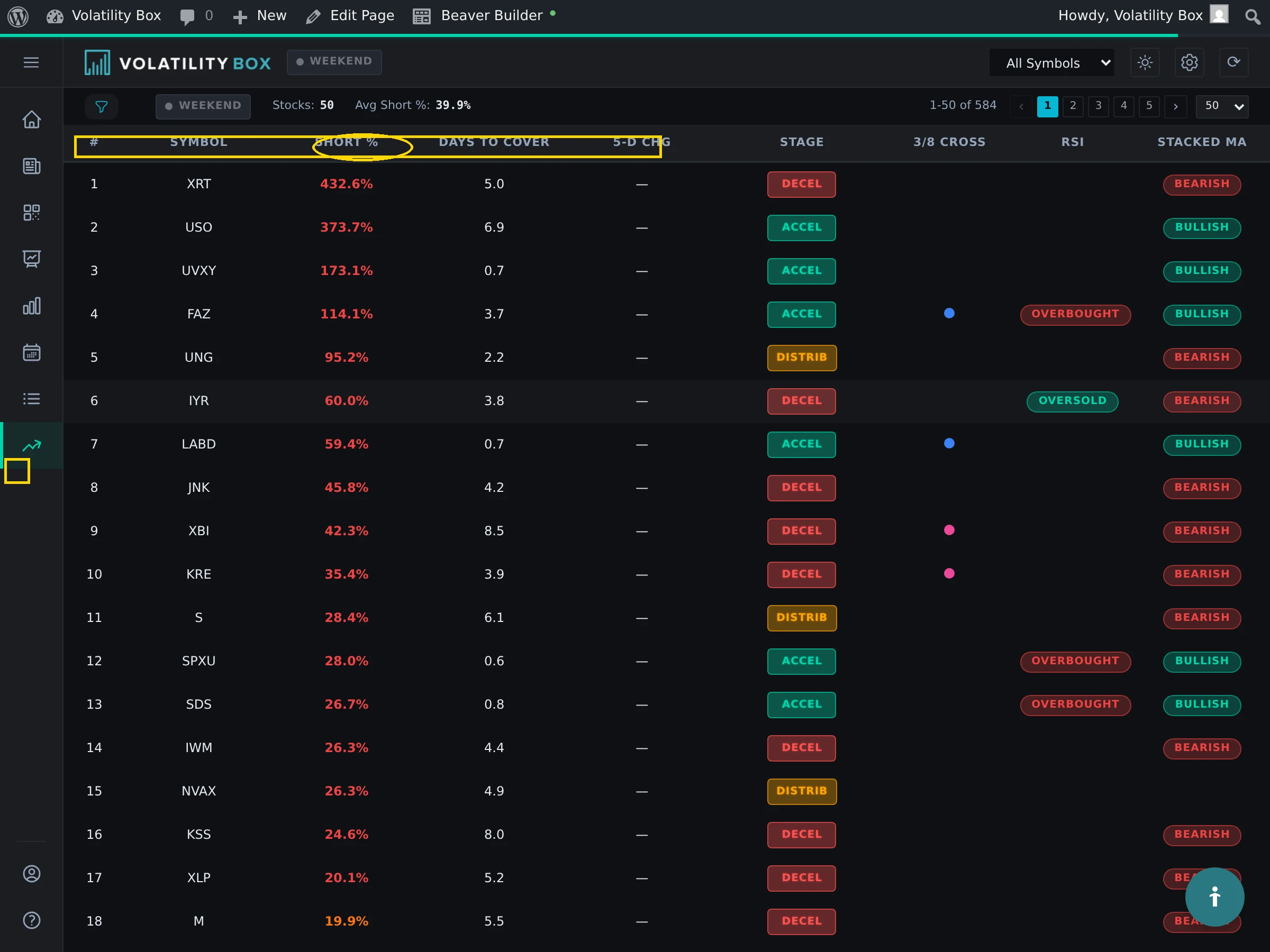

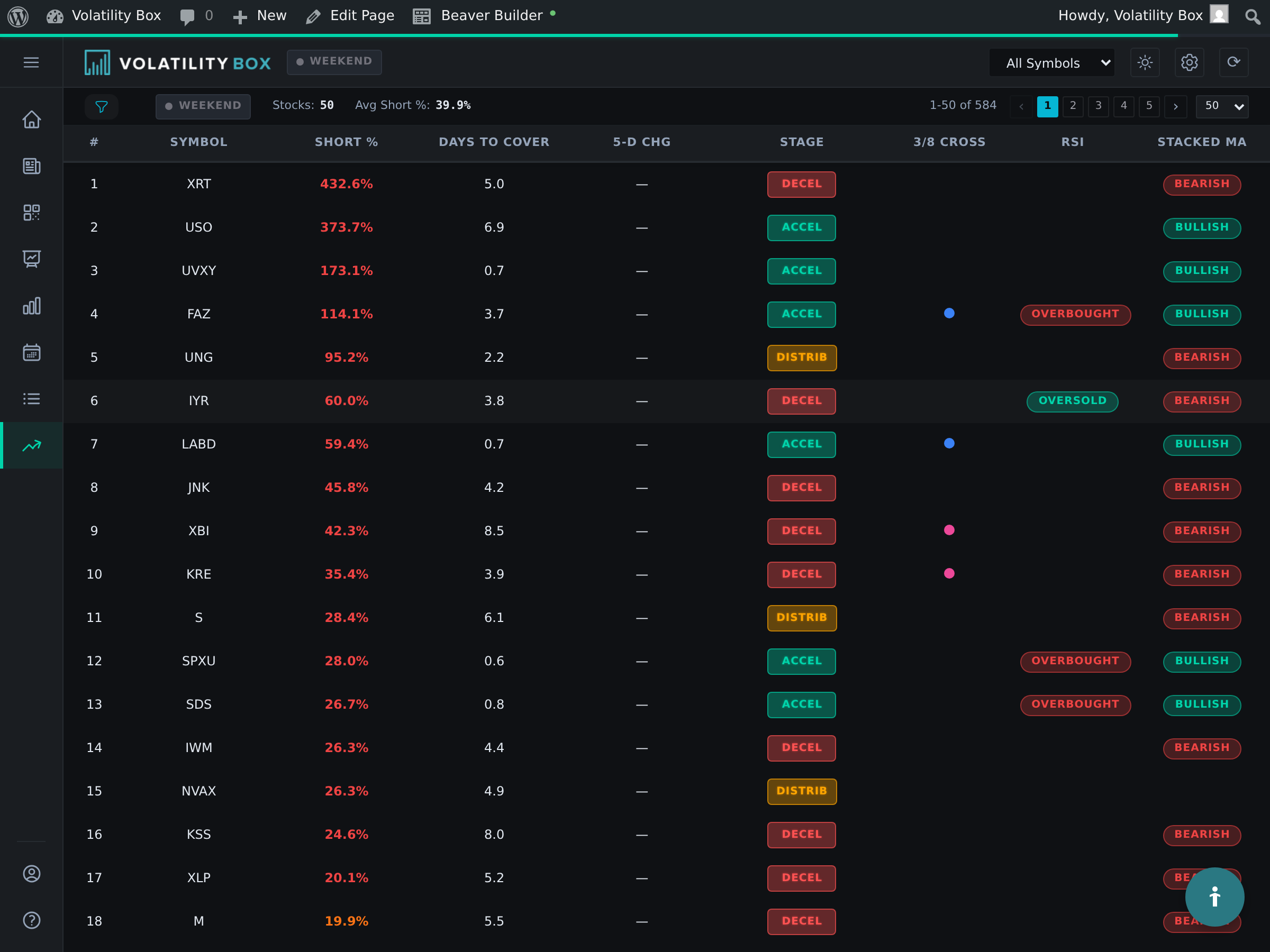

Accessing the Short Interest Scanner

The Volatility Box platform includes a dedicated Short Interest Scanner that displays real-time short interest data for the supported universe of stocks. To access it, navigate to the Short Interest tab in the main sidebar menu.

The scanner displays stocks sorted by short interest percentage by default. This integrated scanner eliminates the need to visit external websites or manually compile short interest data from multiple sources.

The Short Interest Scanner updates twice monthly based on official FINRA reporting schedules, typically around the 15th and last day of each month. While the data has a 1-2 week lag inherent to regulatory reporting, it’s sufficient for identifying stocks with persistently high short interest. The scanner covers the same 595 supported stocks as the main Volatility Scanner, ensuring consistency across the platform.

Float Calculation and Availability

The float is the number of shares actually available for public trading. It’s calculated by taking total shares outstanding and subtracting restricted shares (locked up in employee stock options or under SEC restrictions) and insider holdings (shares held by founders, executives, and board members).

For example, a stock might have 100 million shares outstanding on paper, minus 20 million restricted shares, minus 30 million insider holdings. This results in a float of only 50 million shares actually available for public trading.

Float size matters enormously for squeeze potential. Smaller float makes squeezes dramatically easier and more violent. If 20 million shares are sold short and the float is only 50 million shares, that represents 40% of all available shares currently held in short positions.

When price starts rising unexpectedly, shorts scramble to buy shares to cover their losses. They’re all competing simultaneously for a limited pool of available shares. This drives the price higher through competitive bidding and triggers more forced covering in a self-reinforcing feedback loop.

High squeeze potential typically requires float below 50 million shares combined with short interest above 20%.

Days to Cover Metric

Days to Cover (DTC) estimates how many days it would theoretically take for all short sellers to cover their positions at the stock’s average daily trading volume. The formula is: Days to Cover = Shares Sold Short / Average Daily Volume.

For example, if 12 million shares are sold short and average daily volume is 2 million shares, DTC equals 12M / 2M = 6 days. This means it would theoretically take 6 full trading days of average volume for all shorts to exit their positions.

DTC thresholds indicate different levels of squeeze risk:

- Below 3 days: Low squeeze risk since shorts can cover quickly without major price disruption

- 3-5 days: Moderate squeeze risk with some covering pressure possible if price rallies

- 5-10 days: High squeeze risk where shorts are significantly trapped if price rallies

- Above 10 days: Extreme squeeze risk with massive explosive potential

The sweet spot for high-probability squeeze trades is DTC greater than 5 days combined with price starting to reverse upward.

Squeeze Mechanics and Cycle

A short squeeze happens when short sellers are forced to buy shares to cover their positions, driving the price higher in a self-reinforcing cycle. The squeeze cycle typically unfolds in eight sequential stages:

- Initial Decline: The stock declines steadily over weeks or months as shorts pile in betting on further downside

- Short Interest Builds: Short interest climbs to 20-30% of float or higher as more traders join the bearish thesis

- Price Reversal: Price reverses unexpectedly due to positive news, technical bounce, or institutional buying

- Shorts Lose Money: Shorts start accumulating unrealized losses that grow daily

- Margin Calls Trigger: Losses exceed account equity thresholds, forcing brokers to demand covering or more capital

- Forced Covering Begins: Shorts buy shares to close positions, pushing price higher

- Panic Covering: More shorts panic and cover as they watch price rising, creating a snowball effect

- Squeeze Peaks: Most shorts have covered, buying pressure exhausts, and price typically collapses

The GME squeeze in January 2021 demonstrates these mechanics perfectly. In early January, GME traded around $20 with short interest at an astounding 140% of float. By January 28, the stock peaked at $483. The entire squeeze lasted approximately 15 days from initial move to final collapse.

Squeeze Triggers

Squeezes require specific catalysts that shift market sentiment and trap overconfident shorts. There are three primary trigger types:

Technical Price Reversal: The stock hits a major support level and bounces hard, catching shorts who expected further downside. For example, a stock might drop from $30 to $18 with short interest climbing to 22%, but at $18 a major support level holds and price bounces sharply to $22.

Positive News Catalysts: Earnings beats, new product launches, analyst upgrades, or partnership announcements that invalidate the bearish thesis. A company might report earnings 64% above expectations, causing the stock to gap 15% higher on the open.

Gamma Squeeze Dynamics: Heavy call option buying forces market makers to buy shares to hedge their exposure. This creates additional buying pressure that accelerates the squeeze. In a gamma squeeze, retail traders buy massive call option volume, market makers must buy shares to hedge, this pushes price higher which puts more calls in-the-money, requiring even more hedging.

AMC in June 2021 demonstrated dramatic gamma squeeze dynamics when massive call option volume forced dealers to buy millions of shares, accelerating the move from $12 to $72 in just days.

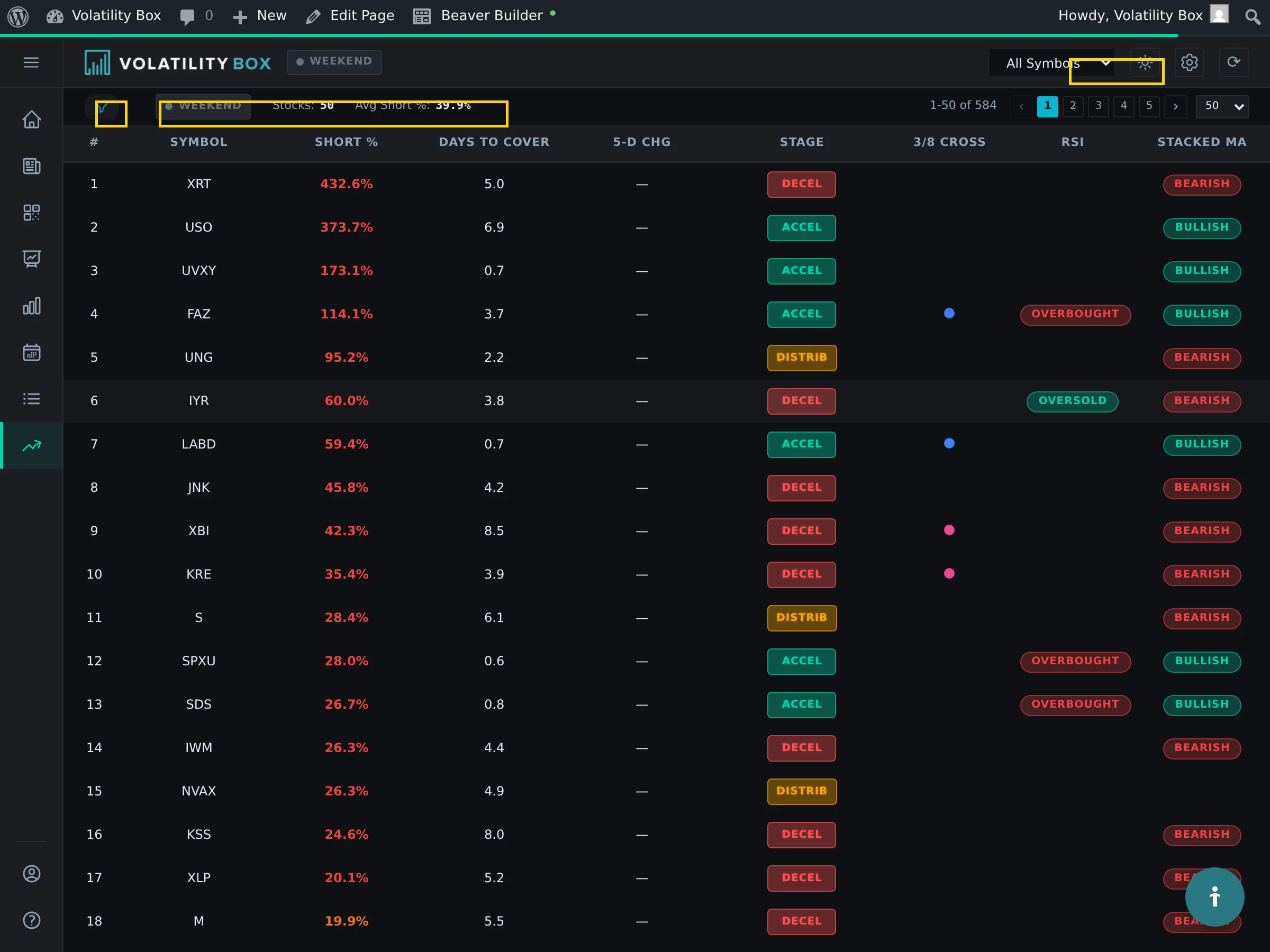

Using Scanner Filters

The Short Interest Scanner includes filtering capabilities that let you narrow down the universe to stocks meeting specific squeeze criteria. You can filter by minimum short interest percentage, Days to Cover, and float size.

A typical filter setup for squeeze candidates:

- Short Interest greater than 20% to ensure substantial short positioning

- Days to Cover greater than 5 to confirm shorts are trapped by low liquidity

- Float less than 200 million shares to focus on stocks with limited supply

Applying these filters typically reduces the universe from 595 stocks down to 10-20 prime squeeze candidates. From there, you can cross-reference with the main Volatility Scanner to identify which candidates have LONG signals with high conviction.

Risk Factors and Fundamentals

Not all high short interest creates good trading opportunities. Sometimes shorts are fundamentally correct and the company is genuinely troubled. A company might be losing substantial money every quarter, facing elevated bankruptcy risk, under regulatory investigation, or losing market share to competitors.

Before trading any potential squeeze, run through this fundamental checklist:

- Is the company profitable or is there a clear path to profitability?

- Is the cash burn rate sustainable?

- Is debt manageable or are they over-leveraged?

- Is revenue growing or at least stable?

- Is there pending bankruptcy or delisting risk?

If you answer no to most of these questions, the short thesis may be fundamentally valid. The stock could genuinely go to zero regardless of technical setup.

Liquidity risk is another major factor. Low-float, heavily-shorted stocks often have wide bid-ask spreads and poor order execution. A stock might be quoted at $25.00 bid / $25.80 ask (an 80 cent spread representing 3.2% slippage). Use limit orders exclusively and never use market orders on squeeze candidates.

Position Sizing for Squeezes

Squeeze trades are inherently higher risk than normal Volatility Box setups due to increased volatility, difficulty predicting the peak, and critical exit timing. For squeeze trades, you should risk only 1% of account value, representing a 50% position size reduction from standard 2% risk.

For example, with a $50,000 account:

- Normal risk: 2% = $1,000 per trade

- Squeeze risk: 1% = $500 per trade maximum

Consider a squeeze setup with entry at $22.00, VB stop at $20.00, and risk per share of $2.00. Position size becomes $500 risk / $2.00 per share = 250 shares maximum. This disciplined sizing prevents any single squeeze trade from damaging your account even if it gaps through your stop.

Short Interest Data Updates

Understanding the data update schedule helps you know when to check for new opportunities. Short interest data in the Volatility Box Scanner updates twice monthly based on FINRA settlement dates, typically around mid-month and month-end.

The data is always 1-2 weeks old by the time you see it due to regulatory reporting lags. This inherent lag is a limitation you must understand when trading squeezes.

Despite the data lag, sudden price movements and volume spikes often indicate significant short covering or short buildup before official data confirms the change. Pay attention to price action and volume as leading indicators. If a stock with 25% short interest suddenly rallies 30% on massive volume over 3 days, you can reasonably assume substantial short covering occurred.

Use the scanner data as a starting point for identifying candidates, but rely on real-time price action and VB signals for actual trade timing.

When to Avoid Squeezes

Skip potential squeeze setups when these red flags appear:

- Fundamentals are terrible: The company is losing money with no path to profit

- Short interest below 15%: Not enough trapped shorts to generate meaningful pressure

- Days to Cover less than 3: Shorts can cover quickly without major price impact

- No technical reversal pattern: Hoping for a squeeze without proper setup is gambling

- Stock already up 50%+ from lows: You’re likely late and the squeeze may be ending

- Emotional state: Feeling FOMO or revenge trading leads to poor decisions

Next Steps

To get started with the Short Interest Scanner:

- Click the Short Interest tab in the sidebar and sort by Short % with highest values first

- Check Days to Cover for each symbol and look for Short % greater than 20% AND Days to Cover greater than 5

- Cross-reference promising symbols with the main Volatility Scanner to find those with LONG signals

- Research fundamentals of any candidates before entering a position

Remember that squeeze trading is advanced and carries significantly higher risk than standard setups. Don’t trade them with real money until you’re consistently profitable on standard VB setups.

Was this article helpful?

Still need help?

Can't find what you're looking for? Our support team is here to help.

Contact Support