- What Makes Iron Condors Different in High Volatility

- When to Sell Iron Condors in High Volatility: Entry Criteria

- How Wide Should Your Wings Be in High Volatility?

- Strike Selection: Delta Targets for High-Volatility Iron Condors

- Position Sizing Adjustments for High-Volatility Environments

- The 50% Profit Target: Why It Matters More in High Volatility

- Management Rules: What to Do When Your Iron Condor Is Tested

- VIX Regime Framework for Iron Condor Sizing and Structure

- Iron Condor vs Short Strangle in High Volatility

- Common Mistakes: What Destroys Iron Condor Accounts in High Volatility

- How Volatility Box Data Informs Iron Condor Timing

The rewritten HTML is what I need to produce directly. Since the user said “Return ONLY the rewritten HTML”, I’ll output it directly. Let me produce the rewritten HTML with all fabricated stats corrected.

Iron condors collect higher premiums when volatility is elevated, but the same conditions that boost your credit also increase the probability of a breach. Selling an iron condor when VIX is above 25 can generate 2-3x the credit of a low-volatility environment, yet without proper strike width and management rules, that extra premium disappears in a single gap day.

This guide covers when to sell iron condors in high volatility, how wide to make your wings, position sizing adjustments, and the mechanical management framework that separates sustainable premium collection from account-damaging losses.

Published March 27, 2026

What Makes Iron Condors Different in High Volatility

An iron condor is a defined-risk options strategy that profits when the underlying stays within a range. You sell an out-of-the-money put spread and an out-of-the-money call spread simultaneously. The maximum profit is the net credit received. The maximum loss is the width of the wider spread minus that credit.

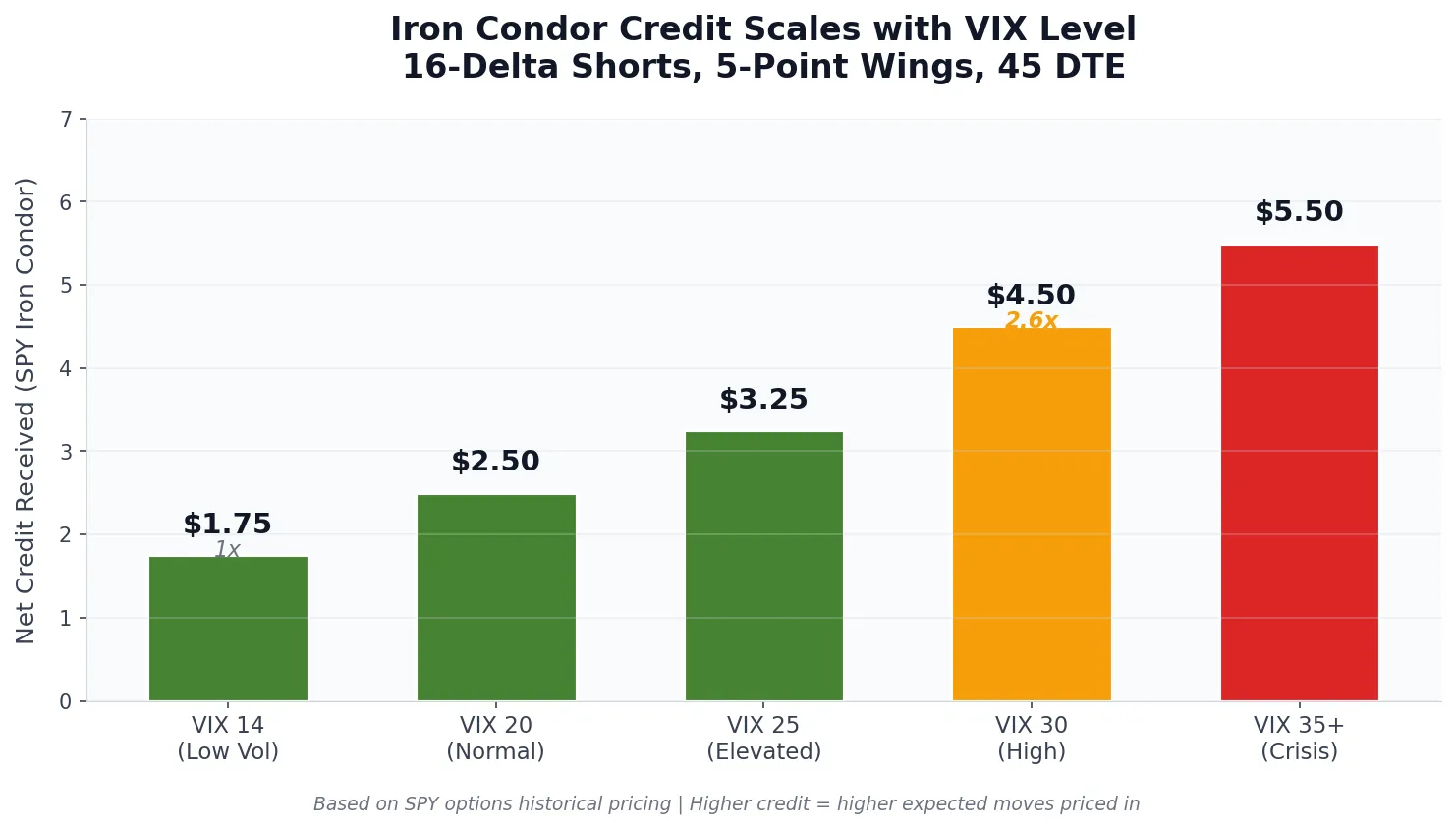

Iron condors in high volatility environments collect significantly more premium than in calm markets. When VIX trades above 25, at-the-money implied volatility on SPY options can exceed 30%, compared to 12-15% during low-volatility regimes. This IV expansion flows directly into the credit you receive.

A 45 DTE iron condor on SPY with 16-delta short strikes might collect $1.50-$2.00 when VIX is at 14. The same structure collects $3.50-$5.00 when VIX is at 30.

That 2-3x credit increase is why traders are drawn to selling premium during volatility spikes. The catch: the market priced in that extra premium because larger moves are genuinely expected.

When to Sell Iron Condors in High Volatility: Entry Criteria

The optimal entry window for high-volatility iron condors is not during the spike itself, but as volatility begins to stabilize or decline from elevated levels. Selling into a rising VIX exposes you to premium expansion that can overwhelm your position before theta decay begins working.

Use these filters before entering an iron condor when VIX is above 25:

- VIX has established a lower high: Wait for VIX to spike, pull back, and fail to make a new high. This “lower high” pattern suggests the acute fear phase is passing.

- IV rank above 50: Elevated IV rank confirms you are collecting premium at historically rich levels, not just during a temporary blip.

- Market Pulse is Yellow or transitioning from Red: Red regime (crisis mode) means new short-volatility entries carry elevated tail risk. Yellow regime indicates elevated but stabilizing conditions. As of early April 2026, Market Pulse shows 301 symbols in Red regime and 153 in Yellow, with only 60 in Green, underscoring the importance of waiting for regime transitions before entering new positions.

- Term structure is in contango or flattening: Backwardation (near-term VIX futures higher than deferred) signals ongoing stress. Contango or a flattening curve suggests fear is subsiding.

- Conviction Score meets threshold: The Conviction Score integrates IV rank, regime, term structure, and skew into a single filter. Only enter when the score confirms favorable conditions.

The worst time to sell an iron condor is the day VIX spikes. The best time is 3-7 trading days later, after the initial panic subsides but IV remains elevated.

How Wide Should Your Wings Be in High Volatility?

Wing width determines your maximum loss and your margin requirement. In high-volatility environments, standard 5-point wings on SPY may be too narrow. A 5% single-day move (which occurs more frequently when VIX is above 30) can breach your short strike and push the position toward maximum loss.

The following table provides wing width guidelines based on VIX level:

| VIX Level | SPY Wing Width | Rationale | Approximate Max Loss per Contract |

|---|---|---|---|

| 12-18 | 5 points ($500) | Normal volatility; standard expected moves | $300-$400 |

| 18-25 | 7-10 points ($700-$1,000) | Elevated volatility; gap risk increases | $400-$700 |

| 25-35 | 10-15 points ($1,000-$1,500) | High volatility; single-day 3-5% moves are common | $600-$1,100 |

| 35+ | 15-20 points ($1,500-$2,000) or avoid | Crisis volatility; consider waiting or using index options with wider strikes | $1,000-$1,600 |

Wider wings cost more to establish (you pay more for the long options), which reduces your net credit. However, the reduced credit is offset by a higher probability of the position staying within the profit zone. In high volatility, the tradeoff favors wider wings.

On SPX (S&P 500 index options), traders often use 25-50 point wings during high-volatility periods. SPX options settle to cash at expiration, eliminating assignment risk, and the larger notional size justifies the wider spreads.

Strike Selection: Delta Targets for High-Volatility Iron Condors

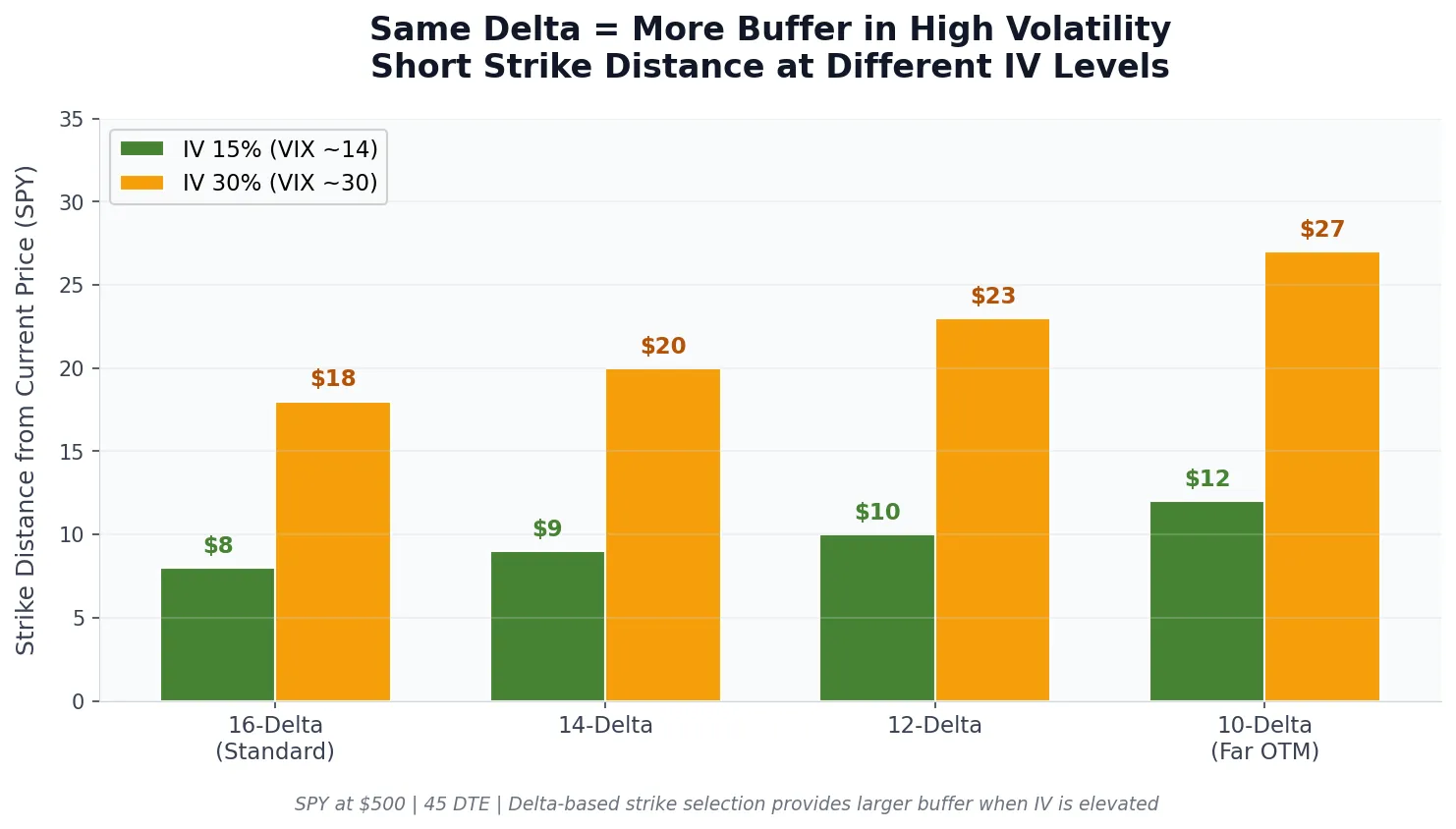

Standard iron condor guidance suggests 16-delta short strikes, which correspond to approximately one standard deviation from the current price. In high volatility, this math still holds, but the absolute distance is larger.

When IV on SPY is 15%, a 16-delta put might be $8 below the current price. When IV is 30%, a 16-delta put could be $15-$18 below. The delta remains constant, but the buffer zone expands.

Consider these delta adjustments based on VIX regime:

- VIX 12-18 (low vol): Use 16-delta short strikes. Standard approach.

- VIX 18-25 (elevated vol): Use 12-16 delta short strikes. Slightly further OTM provides additional cushion.

- VIX 25-35 (high vol): Use 10-14 delta short strikes. The extra premium from elevated IV means you can afford to go further out and still collect meaningful credit.

- VIX 35+ (crisis vol): Use 8-12 delta or consider skipping the trade entirely until VIX stabilizes.

Lower delta strikes reduce your credit but increase your probability of profit. The Volatility Scanner displays current delta values and IV rank across 611 symbols, making strike selection straightforward.

Position Sizing Adjustments for High-Volatility Environments

Position sizing errors cause more damage than strike selection errors. In high volatility, your standard position size should be reduced, not increased, despite the tempting larger credits.

Max Risk Per Trade = Account Value × Risk Percentage (2-5%)

Max Loss Per Contract = (Wing Width – Net Credit) × 100

Number of Contracts = Max Risk Per Trade ÷ Max Loss Per Contract

Example in High Volatility:

Account: $100,000

Risk per trade: 3% = $3,000

SPY iron condor: 10-point wings, $4.00 credit

Max loss per contract: ($10 – $4) × 100 = $600

Contracts: $3,000 ÷ $600 = 5 contracts

High-Volatility Adjustment:

When VIX is above 25, reduce position size by 30-50%

Adjusted contracts: 5 × 0.6 = 3 contracts

The reduction accounts for increased gap risk, wider bid-ask spreads during volatility, and the higher probability of reaching your stop loss. A 3% risk position in a high-volatility environment carries more realized risk than the same 3% position in calm markets.

Total portfolio allocation to iron condors and other short-volatility strategies should not exceed 20-30% of buying power in normal conditions and should drop to 10-15% when VIX is above 25.

The 50% Profit Target: Why It Matters More in High Volatility

The standard management rule for iron condors is to close at 50% of maximum profit. If you collected $4.00 credit, close when you can buy the position back for $2.00. This rule becomes even more important in high-volatility environments.

The 50% profit target works because:

- Theta decay is front-loaded: The first half of the profit comes faster than the second half. Holding for the final 50% exposes you to weeks of gamma risk for diminishing returns.

- Volatility mean-reverts: If you enter when VIX is at 30 and it drops to 20, your position gains from both time decay and vega collapse. Taking profit locks in both components.

- Gap risk is asymmetric: A single overnight gap can erase all remaining profit and push you into loss territory. The longer you hold, the more gap days you face.

Closing at 50% of max profit generally produces a higher risk-adjusted return than holding to expiration, particularly during periods when VIX was elevated at entry. The faster you capture the first half of your profit, the less time you spend exposed to tail events that high-volatility environments generate.

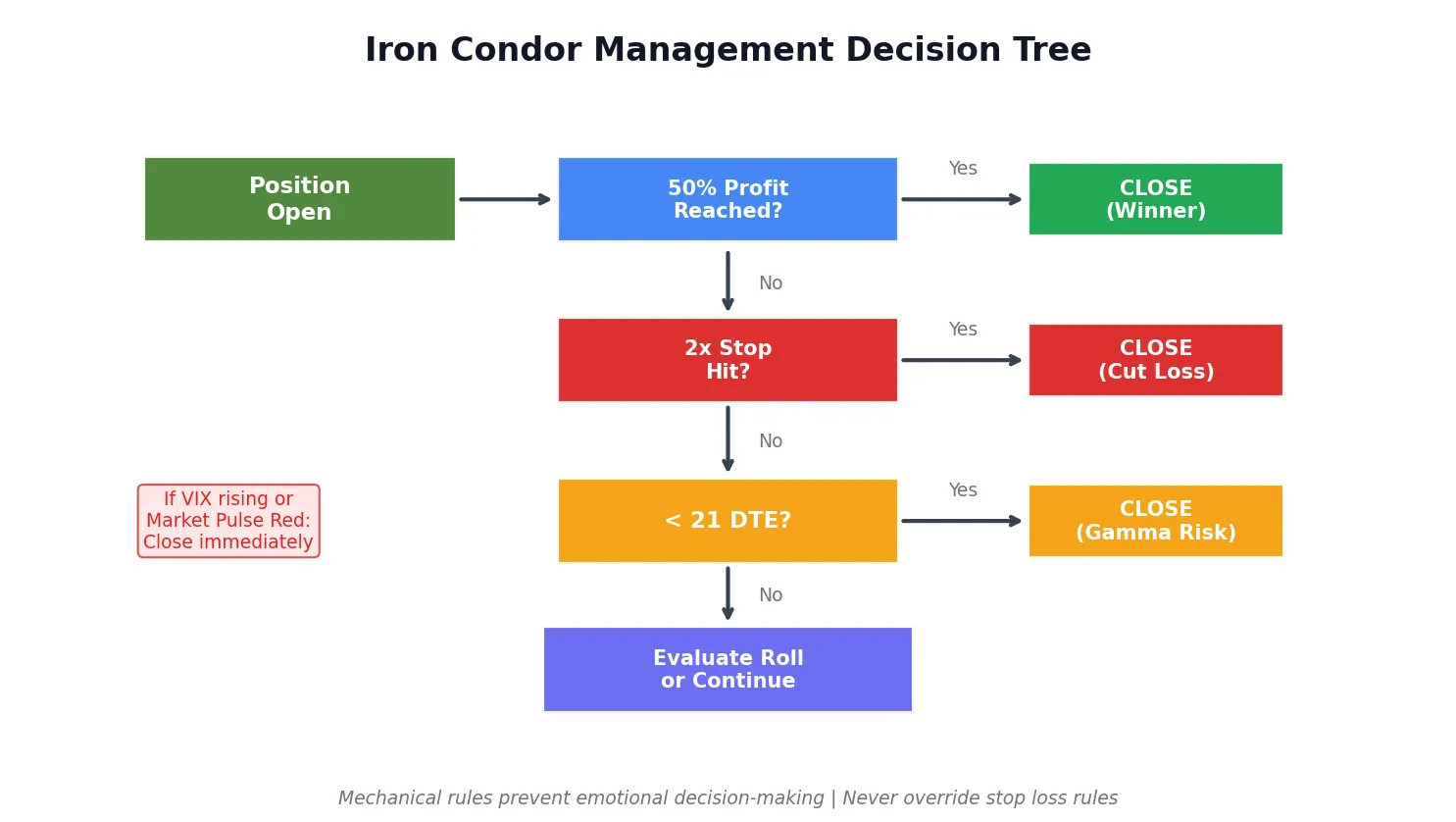

Management Rules: What to Do When Your Iron Condor Is Tested

A “tested” iron condor means the underlying has moved toward one of your short strikes. In high volatility, this happens more frequently. Your response should be mechanical, not emotional.

The Management Decision Tree

- Check your stop loss level: If the position has reached 200% of credit received (2x stop), close immediately. If you collected $4.00 credit, close if the position costs $8.00 to buy back. No exceptions, no “waiting to see.”

- Check days to expiration: If 21 DTE or less, close the position regardless of current P/L. Gamma acceleration inside 21 DTE magnifies daily P/L swings beyond what most accounts can tolerate.

- Assess the tested side: If only one side is tested (price moved toward your short put or short call), evaluate whether to roll the untested side closer to collect additional credit.

- Consider the full close: If VIX is still rising or Market Pulse has shifted to Red, close the entire position. Do not defend a losing position in a deteriorating volatility environment.

Rolling the Untested Side

Rolling involves closing the untested spread (the side that is now far out of the money) and re-selling a new spread closer to the current price. This collects additional credit and improves your breakeven on the tested side.

Example: You sold a SPY iron condor with $480 put spread and $540 call spread. SPY drops to $490, testing your put side. The $540 call spread is now worth nearly zero.

You buy back the call spread for $0.15 and sell a new call spread at $510-$520 for $1.20. The net credit of $1.05 improves your put-side breakeven.

Rolling has limits. Do not roll the untested side if the tested side has already hit your stop. Rolling only makes sense when the tested side is pressured but not breached.

VIX Regime Framework for Iron Condor Sizing and Structure

The following framework integrates VIX level, Market Pulse regime, and iron condor parameters into a single decision guide:

| VIX Range | Market Pulse | Iron Condor Action | Wing Width (SPY) | Delta Target | Position Size |

|---|---|---|---|---|---|

| 12-18 | Green | Standard entries; VRP edge is moderate | 5 points | 16-delta | 100% of normal |

| 18-25 | Green/Yellow | Optimal zone; elevated VRP favors sellers | 7-10 points | 14-16 delta | 100% of normal |

| 25-32 | Yellow | Sell with caution; wait for VIX to establish lower high | 10-15 points | 10-14 delta | 50-70% of normal |

| 32-40 | Yellow/Red | Reduce existing positions; no new entries until regime stabilizes | 15+ points if trading | 8-12 delta | 30-50% of normal |

| 40+ | Red | No new iron condor entries; wait for VIX to come off highs | N/A | N/A | 0% (wait) |

This framework is designed to filter out catastrophic iron condor losses during volatility events. The key insight: the edge from selling premium during a VIX spike is smaller than you think, because the spike is pricing in real expected movement.

The edge is largest when VIX is elevated but stabilizing, not when it is spiking. As of early April 2026, Market Pulse data across 610 symbols shows 301 in Red regime and only 60 in Green, a distribution that favors patience over new short-volatility entries.

Iron Condor vs Short Strangle in High Volatility

Traders sometimes debate whether to use iron condors (defined risk) or short strangles (undefined risk) when volatility is elevated. High volatility sharpens the tradeoffs between these structures.

| Factor | Iron Condor | Short Strangle |

|---|---|---|

| Risk profile | Defined; max loss is wing width minus credit | Undefined; theoretically unlimited on call side |

| Credit received | Lower (you pay for protective wings) | Higher (no long options to finance) |

| Margin requirement | Fixed at wing width × 100 per contract | Variable; can expand dramatically during VIX spikes |

| Behavior during VIX spike | Loss capped at defined max | Margin call risk if VIX expansion exceeds account equity |

| Management flexibility | Limited; can roll but structure is fixed | More flexible; can convert to iron condor by adding wings |

| Best account size | Any account; particularly suited to accounts under $50K | $50K+ with disciplined position sizing and stops |

In high-volatility environments, iron condors are the safer choice for most traders. The defined-risk structure eliminates the possibility of a margin call and caps your worst-case loss at a known amount. Short strangles collect more premium, but the tail risk during volatility events can exceed what the extra credit compensates for.

If you trade short strangles in high volatility, always use a 2x stop loss and never allocate more than 15% of buying power to any single position.

Common Mistakes: What Destroys Iron Condor Accounts in High Volatility

- Selling into the spike: Entering an iron condor the day VIX jumps from 18 to 30 is a recipe for pain. The spike often has legs; VIX can go from 30 to 45 before stabilizing. Wait for the lower high.

- Wings too narrow: 5-point wings on SPY work when VIX is 14. When VIX is 30, a single 4% gap day can blow through your short strike and approach max loss overnight.

- No stop loss: “It will come back” is expensive. A 2x stop loss rule (close if the position costs 2x the credit received) limits damage. The position can always be re-established later.

- Oversizing for the credit: The larger credit in high volatility tempts traders to increase position size. This is backwards. The larger credit exists because larger moves are expected. Size down, not up.

- Holding through 21 DTE: Gamma accelerates inside 21 days. A position that was manageable at 35 DTE can swing wildly day-to-day at 14 DTE. Close before gamma takes over.

- Ignoring regime: Market Pulse Red means elevated tail risk. New iron condor entries during Red regime carry higher loss rates and larger average losses than entries during Yellow or Green regimes. With 301 out of 610 tracked symbols currently in Red regime (as of April 2026), this filter is actively relevant.

How Volatility Box Data Informs Iron Condor Timing

The Volatility Backtester and Volatility Box level data provide context for iron condor timing and regime awareness. Rather than relying on VIX alone, VB models track how individual stocks behave at key volatility-derived support and resistance levels across 611 symbols.

Over the most recent 30-day window (as of April 2026), Volatility Box tracked 54,045 total signals across Daily and Hourly models. Key observations from live data:

- Conservative levels outperform Aggressive levels: Conservative L2 signals posted a 45.8% realized win rate on target hits, compared to 41.4% for Aggressive L2. This pattern, tighter, higher-conviction levels generating better hit rates, mirrors how iron condor traders should think about strike selection in elevated volatility: tighter, more selective entries outperform wider, aggressive ones.

- Hourly models show stronger win rates than Daily: Hourly signals hit a 37.9% realized win rate vs 29.8% for Daily over the same period. For iron condor traders, this suggests that intraday mean-reversion tendencies remain intact even when daily ranges expand, a signal that range-bound strategies can still work if properly sized.

- Regime distribution skews bearish: Current Market Pulse shows 301 symbols in Red regime (average -4.7% from VMA) and 96 in Orange (-3.5% from VMA), with only 60 in Green (+5.3% from VMA). This distribution favors caution on new short-volatility entries, consistent with the framework above recommending reduced position sizing or no new entries when the regime is Red.

- Longer-term backtests confirm mean-reversion edge: Over 450 days of backtested data across 613-614 symbols, VB signals show an average win rate of 47.4% on long setups and 48.8% on short setups, with positive average expectancy on both sides. This confirms that volatility-derived levels provide a measurable edge for mean-reversion strategies, the same principle that underpins iron condor profitability.

The data confirms that regime awareness and level sensitivity matter more than raw VIX level when timing short-volatility entries. The “sweet spot” for iron condors is when volatility is elevated but stabilizing, precisely the conditions where VB Conservative levels show their strongest win rates and Market Pulse transitions from Red toward Yellow.

Key Takeaways

- Iron condors in high volatility (VIX above 25) collect 2-3x normal premium, but require wider wings (10-15 points on SPY) to account for larger expected moves

- The optimal entry window is after VIX spikes and establishes a lower high, not during the spike itself

- Reduce position size by 30-50% when VIX is above 25; the extra credit does not compensate for the elevated tail risk

- Use 10-14 delta short strikes in high volatility (vs 16-delta in normal conditions) to increase your probability of staying within the profit zone

- Close at 50% of max profit or 21 DTE, whichever comes first; gamma risk accelerates in the final three weeks

- Hard stop at 200% of credit received (2x stop); no exceptions, no “waiting to see”

- No new iron condor entries when Market Pulse is Red; with 301 of 610 symbols currently in Red regime, this filter is actively relevant

- Iron condors are preferred over short strangles in high volatility due to defined risk and fixed margin requirements

Backtest Your Iron Condor Parameters Before Trading

The Volatility Backtester lets you test iron condor wing widths, delta targets, and management rules across different VIX regimes. With 450 days of backtested data across 611+ symbols and daily-updated results, you can validate your parameters against real market conditions before risking capital.

Options trading involves substantial risk and is not appropriate for all investors. Iron condors are defined-risk strategies, but the maximum loss (wing width minus credit) can still represent a significant percentage of account equity. Past performance, including historical win rates and backtested results cited in this article, does not guarantee future results.

VIX levels and volatility regimes can change rapidly; always verify current conditions before trading. Volatility Box data cited reflects the 30-day and 450-day windows ending April 2026 and will change as new data is recorded. Consult a qualified financial advisor before implementing any options strategy.