- What Are 0DTE Options and Why Do They Matter for Volatility Traders

- How 0DTE Implied Volatility Differs from Longer-Dated Options

- The Gamma Effect: Why 0DTE Options Move Markets

- How Theta Decay Works on Expiration Day

- Which Volatility Conditions Favor 0DTE Trading

- 0DTE Options Strategies: Directional and Volatility-Based Approaches

- Position Sizing for 0DTE Options: The 1% Rule

- When to Enter 0DTE Trades: Timing Windows and Volatility Cycles

- How VIX and VIX1D Readings Inform 0DTE Decisions

- Managing Risk: Stop Losses and Time Exits for 0DTE

- 0DTE Options and Volatility Box: Using Hourly Models for Same-Day Trades

- Common Mistakes in 0DTE Volatility Trading

Zero-days-to-expiration options now account for 59% of total SPX options volume, transforming intraday volatility trading from a niche strategy into a structural market force. The average 0DTE SPX option moves 200-400% on a 1% index move, compared to 40-80% for weekly options with similar deltas. This leverage, combined with same-day expiration and the absence of overnight risk, creates a trading environment where volatility itself becomes the primary edge. Understanding how implied volatility behaves on expiration day, when gamma peaks, and how to size positions for instruments that can move 500% in minutes is the foundation of profitable 0DTE trading.

Published March 20, 2026

What Are 0DTE Options and Why Do They Matter for Volatility Traders

0DTE options are options contracts that expire on the same day they are traded. The term “zero days to expiration” describes the exact condition: the contract will be worthless or exercised by the closing bell. On SPX and SPY, 0DTE options are now available every trading day following the CBOE’s expansion of daily expirations in 2022.

The volatility characteristics of 0DTE options differ significantly from standard weekly or monthly options. Time value has compressed to hours rather than days. Theta decay accelerates exponentially through the session. Gamma reaches levels impossible in longer-dated contracts, making delta hedging by market makers the primary driver of intraday price swings.

For volatility traders, 0DTE options represent both the purest expression of intraday volatility and a tool for positioning around it. A trader who understands the volatility regime, measured through Market Pulse and real-time VIX readings, can select 0DTE strikes that capture directional moves with defined risk. The key is matching the option’s characteristics to the expected volatility environment.

How 0DTE Implied Volatility Differs from Longer-Dated Options

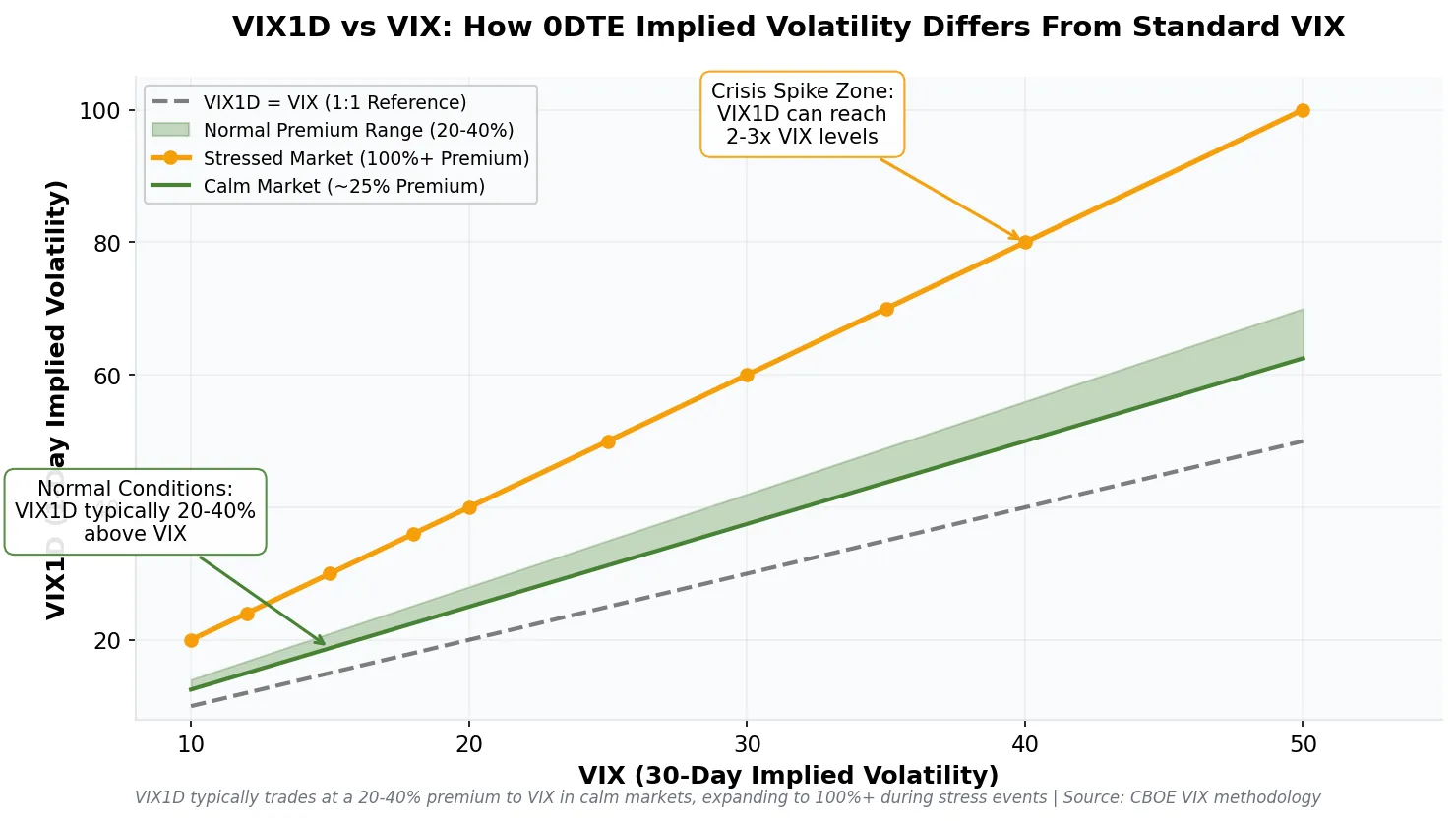

Implied volatility on 0DTE options behaves unlike any other expiration cycle. The VIX measures 30-day expected volatility, but 0DTE options price volatility for the remaining hours of the session only. This creates a unique implied volatility structure that spikes at the open, compresses through midday, and expands again into the close.

The VIX1D index, introduced by the CBOE in 2023, measures one-day expected volatility using 0DTE SPX options. VIX1D typically trades at a 20-40% premium to VIX during calm markets, reflecting the concentration of uncertainty into a single session. During high-volatility regimes, VIX1D can spike to 2-3x the VIX level as traders bid up same-day protection.

| Metric | 0DTE Options | Weekly Options (5-7 DTE) | Monthly Options (20-30 DTE) |

|---|---|---|---|

| Implied Volatility Source | VIX1D (1-day) | VIX9D / VIX (blended) | VIX / VIX3M (blended) |

| IV Premium to VIX | +20-40% (calm), +100-200% (stressed) | +5-15% | Baseline (VIX reference) |

| Theta Decay Rate | $0.05-$0.50/hour (ATM) | $0.01-$0.05/hour | $0.002-$0.01/hour |

| Gamma at ATM | 0.15-0.40 (extremely high) | 0.03-0.08 | 0.01-0.03 |

| Delta Sensitivity to IV | High (vanna effect pronounced) | Moderate | Low |

| Overnight Risk | None (expires same day) | Moderate | High |

The practical implication: 0DTE IV cannot be assessed using standard VIX readings. A VIX of 15 might correspond to 0DTE ATM implied volatility of 18-22 in the morning and 12-14 by 2:00 PM as time value evaporates. Traders who price 0DTE options using VIX as a proxy consistently misprice the actual volatility embedded in the contracts.

The Gamma Effect: Why 0DTE Options Move Markets

Gamma measures how much an option’s delta changes for a one-point move in the underlying. For 0DTE ATM options, gamma reaches levels of 0.15-0.40, compared to 0.02-0.05 for monthly options. This means the option’s delta changes by 15-40 percentage points for every 1% move in SPX.

Market makers who sell 0DTE options must continuously hedge their gamma exposure. When they are short gamma (the typical position), a move in either direction forces them to buy high and sell low to maintain delta neutrality. This mechanical hedging amplifies price moves and creates the “gamma spiral” phenomenon observed on high-volume 0DTE days.

Market maker sells 10,000 SPX 5100 calls at $2.00 (delta 0.50, gamma 0.25)

Initial hedge: Buy 5,000 SPX futures (500,000 delta)

SPX moves from 5100 to 5110 (+10 points):

New call delta = 0.50 + (0.25 x 10) = 0.75

Required hedge = 7,500 futures (750,000 delta)

Action: Buy 2,500 additional futures to stay hedged

This buying pressure pushes SPX higher, increasing delta further, requiring more buying.

Result: Gamma hedging amplifies the initial move.

The gamma effect is most pronounced at specific times. From 2:00-3:30 PM ET on 0DTE days, gamma exposure concentrates around the strikes with the highest open interest. As expiration approaches and time value collapses, gamma spikes to its maximum, and market maker hedging flows become the dominant price driver. The Volatility Scanner tracks real-time gamma exposure levels to identify when these flows are most likely to amplify directional moves.

How Theta Decay Works on Expiration Day

Theta measures the rate at which an option loses value due to time decay. For 0DTE options, theta is not a gradual daily bleed but an hourly collapse. An ATM SPX 0DTE option worth $5.00 at 10:00 AM might be worth $2.50 by 1:00 PM and $0.50 by 3:30 PM, even with zero movement in the underlying.

The theta decay curve on expiration day follows an exponential pattern. Decay is slowest in the first two hours of trading, accelerates through midday, and becomes steepest in the final 90 minutes. By 3:30 PM, an ATM option may lose $0.50-$1.00 per 15-minute period if SPX remains flat.

| Time (ET) | Hours to Expiration | ATM Option Value ($5 at Open) | Theta Decay Rate ($/hour) | Trading Implication |

|---|---|---|---|---|

| 9:30 AM | 6.5 hours | $5.00 | $0.15-$0.25 | Full theta runway; directional bets viable |

| 11:00 AM | 5.0 hours | $4.25 | $0.25-$0.35 | Still adequate time for 1-2 hour trades |

| 1:00 PM | 3.0 hours | $2.80 | $0.40-$0.55 | Theta accelerating; shorter holding periods |

| 2:30 PM | 1.5 hours | $1.50 | $0.60-$0.80 | Scalping only; theta overwhelms small moves |

| 3:30 PM | 0.5 hours | $0.40 | $0.80-$1.20 | Binary outcomes; lottery tickets or hedges |

The theta decay structure creates distinct trading windows. Morning trades (9:30-11:30 AM) have the theta runway to capture multi-hour directional moves. Midday trades (11:30 AM-2:00 PM) work only for scalps or premium selling. Afternoon trades (2:00-4:00 PM) are essentially binary positions where theta has already extracted most of the value. Understanding which window you are trading in determines whether long options or short options strategies are appropriate.

Which Volatility Conditions Favor 0DTE Trading

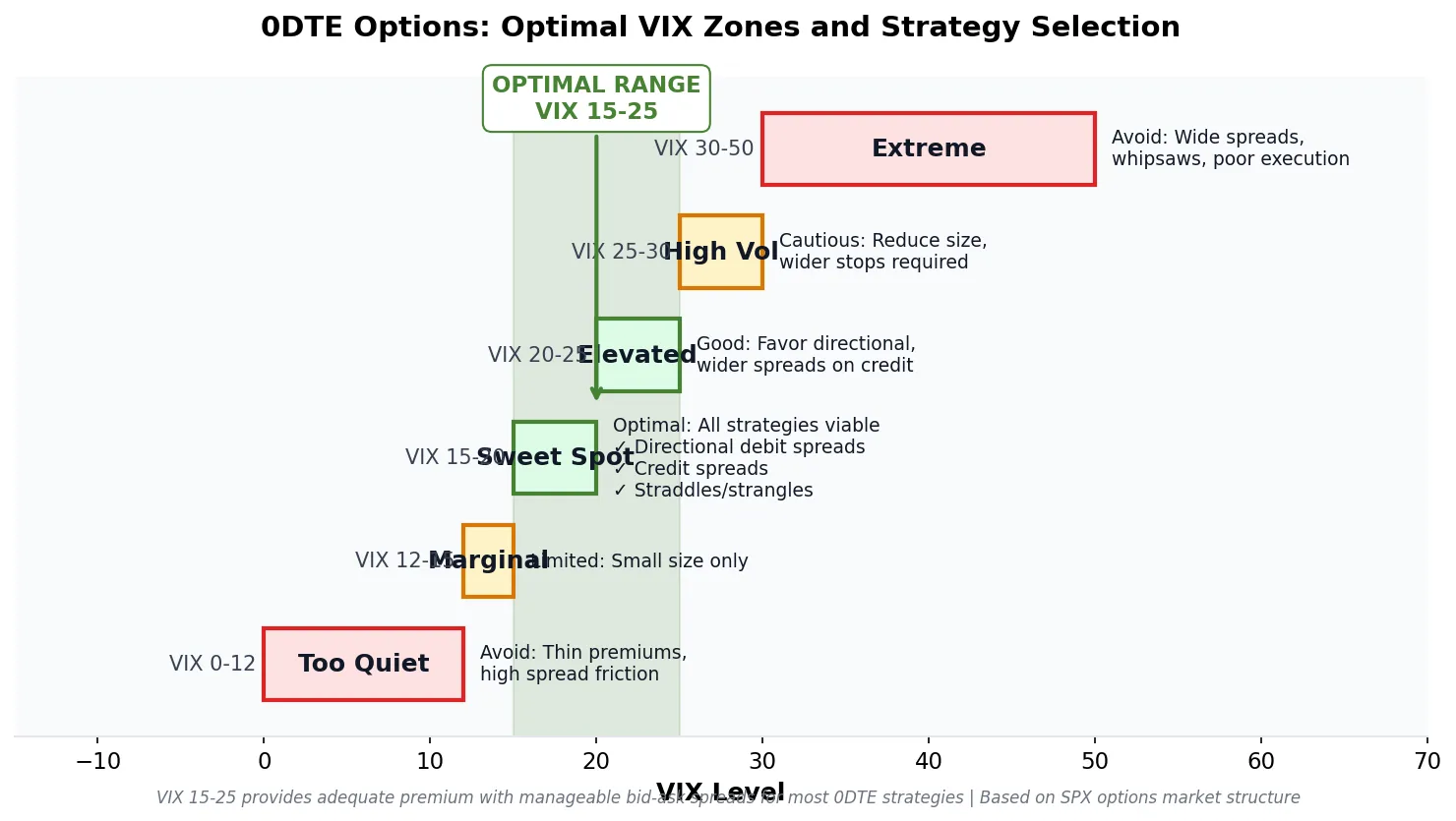

Not every volatility regime supports profitable 0DTE trading. The optimal conditions combine sufficient implied volatility to generate tradeable premiums with realized volatility that matches or exceeds the implied level. When IV exceeds realized volatility by too much, premium sellers win. When realized volatility exceeds IV, directional buyers win.

VIX levels between 15-25 represent the sweet spot for most 0DTE strategies. Below VIX 15, premiums are too thin to justify the transaction costs and bid-ask spreads. Above VIX 30, the extreme premium levels reflect genuine uncertainty, and the wide spreads (often $0.50-$1.00 on SPX 0DTE) make execution difficult. The intermediate range provides adequate premium with manageable spreads.

The Market Pulse regime classification provides context beyond the VIX level. A Green regime (trending, low correlation) favors directional 0DTE trades aligned with the trend. A Yellow regime (choppy, moderate volatility) favors premium selling through 0DTE credit spreads. A Red regime (high correlation, elevated VIX) signals caution; spreads widen, whipsaws increase, and the risk-reward deteriorates for both buyers and sellers.

0DTE Options Strategies: Directional and Volatility-Based Approaches

0DTE trading strategies divide into three categories: directional bets, premium collection, and volatility plays. Each requires different entry timing, position sizing, and exit rules calibrated to the compressed timeframe.

Strategy 1: 0DTE Directional Debit Spreads

Buy a call (or put) spread on 0DTE options to capture a directional move with defined risk. The spread structure reduces the theta drag compared to naked long options. Entry window: 9:45-11:00 AM, after the opening range establishes direction.

Example: SPX trading at 5100, bullish bias. Buy the 5105/5115 call spread for $3.50. Maximum risk = $3.50 per spread. Maximum reward = $6.50 (spread width minus premium). Breakeven = 5108.50. This trade requires SPX to move +8.5 points (0.17%) to profit and +15 points (0.29%) to reach maximum profit. The compressed time value means the spread must be closed by 2:00 PM if the directional thesis has not materialized.

Strategy 2: 0DTE Credit Spreads (Premium Selling)

Sell an out-of-the-money credit spread and let theta decay work in your favor. This strategy profits when SPX stays within a range or moves away from your short strike. Entry window: 10:30 AM-12:30 PM, when theta is accelerating and the opening volatility has subsided.

Example: SPX at 5100, neutral bias. Sell the 5070/5060 put spread for $1.20 credit. Maximum risk = $8.80 (spread width minus credit). Maximum reward = $1.20. The short strike is 30 points (0.59%) below current price. As long as SPX stays above 5070 at expiration, the full credit is retained. The Volatility Box hourly models identify the expected range for the session, allowing traders to place short strikes outside the statistically projected movement.

Strategy 3: 0DTE Straddles and Strangles (Volatility Plays)

Buy or sell ATM straddles (same strike call and put) or OTM strangles (call and put at different strikes) to position for realized volatility versus implied. Long straddles profit when SPX moves more than the premium paid. Short straddles profit when SPX moves less than the premium collected. These are pure volatility trades, not directional bets.

Example: SPX at 5100, expecting higher realized volatility than implied. Buy the 5100 straddle (call + put) for $8.00 combined. The trade profits if SPX moves beyond 5108 or below 5092 (the breakeven range). If expecting compressed volatility, sell the same straddle and profit if SPX stays between the breakevens. The breakeven width as a percentage of SPX (0.16% in this example) provides the volatility hurdle.

Position Sizing for 0DTE Options: The 1% Rule

The extreme leverage of 0DTE options demands strict position sizing. A single 0DTE trade should never risk more than 1-2% of total account capital, regardless of conviction level. The compressed timeframe means there is no opportunity to adjust or hedge after entry; the trade will resolve within hours.

Maximum Risk per Trade = Account Size x 0.01 (1% rule)

Example: Debit Spread

Account: $50,000

Maximum Risk: $50,000 x 0.01 = $500

Spread cost: $3.50 x $100 multiplier = $350 per spread

Maximum contracts: $500 / $350 = 1.4 → trade 1 spread

Example: Credit Spread

Account: $50,000

Maximum Risk: $500

Credit spread max loss: $8.80 x $100 = $880 per spread

Maximum contracts: $500 / $880 = 0.57 → trade 0 spreads (risk too high)

Adjustment: Widen spread to increase credit or find a different setup

The 1% rule prevents catastrophic losses during the inevitable losing streaks. Even five consecutive losing 1% trades leaves 95% of capital intact. Position sizing discipline is more important than strike selection, timing, or volatility assessment. No 0DTE edge survives a single oversized loss.

Account size also determines the appropriate instrument. SPX 0DTE options with $100 multipliers require larger accounts ($25,000+) to trade single spreads within the 1% rule. SPY 0DTE options with $100 multipliers but 1/10th the underlying price allow smaller accounts to participate. XSP (mini-SPX) options provide another alternative for accounts under $25,000.

When to Enter 0DTE Trades: Timing Windows and Volatility Cycles

The optimal entry window for 0DTE trades varies by strategy type and volatility regime. Directional trades favor the post-open window when price discovery is active. Premium-selling trades favor the late-morning window when theta acceleration begins. Volatility plays work best at inflection points where the market is transitioning between regimes.

Window 1: 9:45-10:30 AM (Post-ORB Directional)

The opening range breakout on ES or SPX establishes the session’s directional bias. Once the 15 or 30-minute opening range is defined, 0DTE debit spreads aligned with the breakout direction offer favorable risk-reward. The theta runway is longest during this window, and the directional signal is freshest. Exit by 1:00 PM if the target is not reached.

Window 2: 10:30-11:30 AM (Prime Scalping)

The post-ORB period offers the best balance of remaining theta, established direction, and reduced opening volatility. Directional scalps holding 30-90 minutes work well here. The 5-minute ATR on SPX has typically compressed from its opening peak but remains elevated enough to produce profitable moves. This is the highest-probability window for 0DTE day trading.

Window 3: 11:30 AM-1:30 PM (Midday Premium Selling)

Theta decay accelerates through this window while realized volatility compresses (the U-shaped intraday volatility pattern). Credit spreads sold during this period benefit from both time decay and reduced movement probability. The risk is an afternoon catalyst (Fed speaker, economic data, news event) that creates a late-session volatility expansion.

Window 4: 2:30-3:30 PM (Gamma Scalping)

Advanced traders use the final 90 minutes to scalp gamma as market maker hedging flows intensify. This requires monitoring options flow data, gamma exposure levels, and strike-specific open interest. It is the highest-skill, highest-risk window and is not recommended for traders without real-time options flow tools.

How VIX and VIX1D Readings Inform 0DTE Decisions

The relationship between VIX, VIX1D, and actual 0DTE option pricing provides an edge for informed traders. VIX1D/VIX ratios above 1.3 indicate elevated short-term fear and often precede intraday volatility spikes. Ratios below 1.1 suggest complacency and favor premium-selling strategies.

| VIX1D/VIX Ratio | Market Condition | 0DTE Strategy Implication |

|---|---|---|

| Below 1.0 | Extremely rare; inverted structure | Unusual; investigate cause before trading |

| 1.0-1.1 | Calm; low near-term premium | Favor premium selling; long options cheap |

| 1.1-1.2 | Normal; standard relationship | Both directional and premium strategies viable |

| 1.2-1.3 | Elevated; building near-term uncertainty | Favor directional or hedge with 0DTE |

| Above 1.3 | High; event risk or stress | Wide spreads; reduce size or avoid |

VIX1D spikes intraday more rapidly than VIX because it reflects same-day option pricing. A sudden VIX1D move from 16 to 22 (while VIX moves from 15 to 16) signals that 0DTE options are being bid aggressively for protection. This information arrives before the underlying SPX moves, providing a leading indicator for volatility traders.

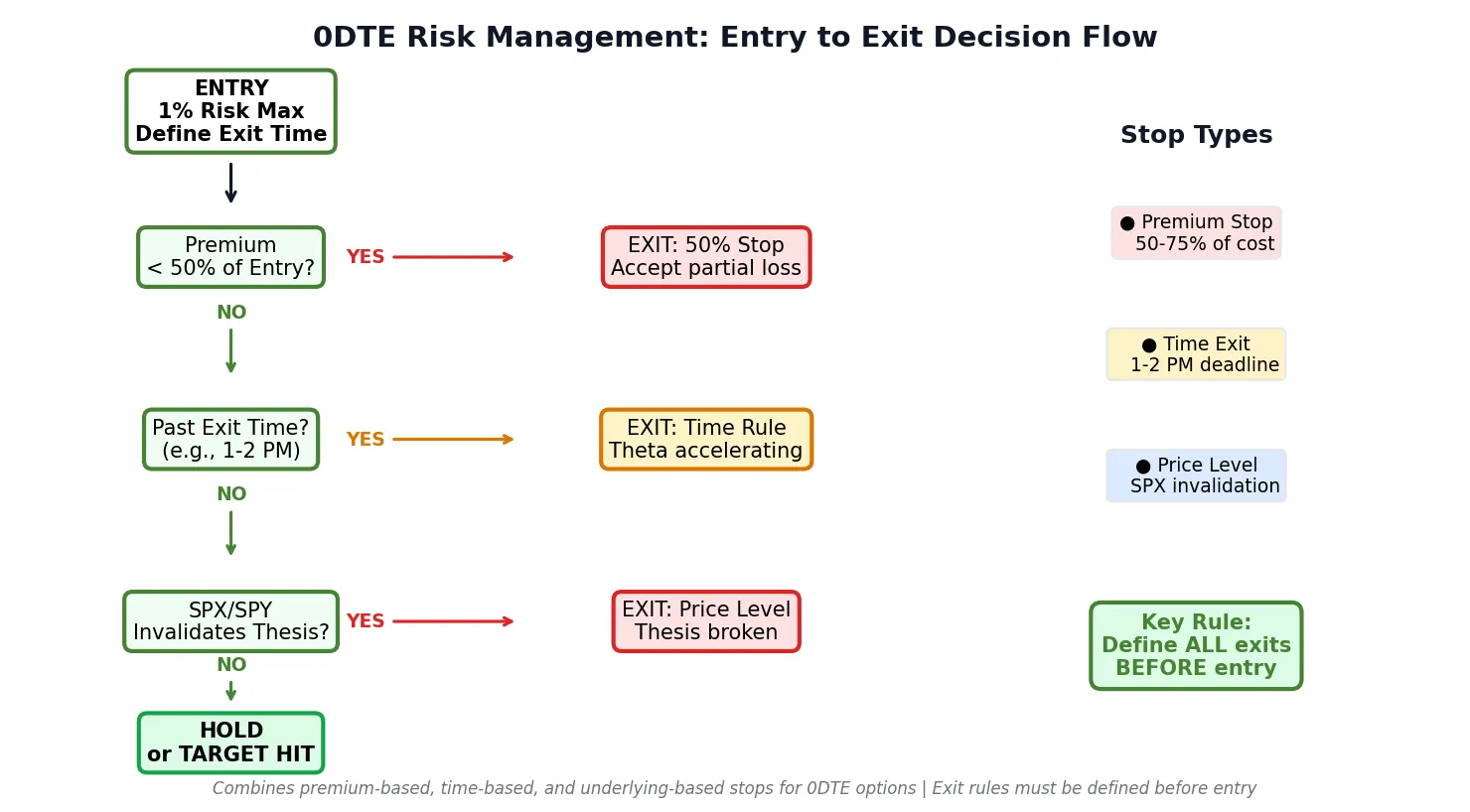

Managing Risk: Stop Losses and Time Exits for 0DTE

Traditional stop-loss mechanics do not translate directly to 0DTE options. The bid-ask spread on SPX 0DTE options ($0.15-$0.50) makes tight stops impractical; a $0.30 stop on a $3.00 spread may trigger from spread fluctuation alone. Instead, 0DTE risk management combines premium-based stops with time-based exits.

Premium-Based Stops

Set a stop at a percentage of premium paid, typically 50-75%. A $4.00 debit spread with a 50% stop exits at $2.00 remaining value (50% loss of premium). This approach accepts that 0DTE options are high-conviction, high-variance trades where partial losses are common.

Time-Based Exits

Define a hard exit time before entry. Directional trades entered before 11:00 AM should exit by 1:00-2:00 PM if the target is not reached. Holding beyond this point converts the trade from a directional bet into a pure theta bleed. Time exits prevent the common failure mode of “hoping” for a late-session move.

Underlying-Based Stops

Use SPX (or SPY) price levels as stop triggers rather than option prices. If the trade thesis requires SPX above 5095, set an alert at 5093 and exit the option position when triggered. This avoids getting stopped out by option market volatility while the underlying remains within the thesis range.

0DTE Options and Volatility Box: Using Hourly Models for Same-Day Trades

The Volatility Box hourly models calculate expected price ranges and key levels that update at the top of each hour. For 0DTE trading, these levels provide statistically derived boundaries for positioning credit spread strikes and evaluating directional breakout probabilities.

The hourly models project a range based on current volatility conditions, volume patterns, and historical behavior at the specific hour of the session. A 10:00 AM hourly model might project SPX range of 5095-5120 for the next 60 minutes, based on the current 5-minute ATR and session context. Credit spread sellers can place short strikes outside this projected range. Directional traders can target the model’s levels as breakout triggers.

The Market Pulse regime indicator adds a qualification layer. During Green regimes, directional breakouts of hourly model levels have higher follow-through probability. During Yellow regimes, fading the levels (selling at the upper boundary, buying at the lower boundary) performs better. During Red regimes, the hourly model ranges expand, and trades require wider stops and smaller size.

Common Mistakes in 0DTE Volatility Trading

- Using VIX as a proxy for 0DTE IV. VIX measures 30-day volatility. 0DTE options price same-day volatility (VIX1D), which trades at a persistent premium and moves independently throughout the session. Check VIX1D, not VIX, for 0DTE pricing context.

- Holding through the theta acceleration window. A directional trade that is not working by 1:00 PM is not going to magically work by 3:00 PM. Theta decay between 1:00-3:00 PM destroys option value faster than most directional moves can recover. Exit unprofitable positions before the final 2 hours.

- Ignoring bid-ask spreads. SPX 0DTE spreads of $0.20-$0.40 represent 5-10% of a typical ATM option’s value. On a $3.00 spread trade, the round-trip cost ($0.40 in and $0.40 out) consumes 27% of the premium. Trade only when the expected move exceeds the spread friction.

- Oversizing because “it’s just one day.” The 1% rule exists because 0DTE trades can lose 100% of premium in hours. A 5% allocation to a losing 0DTE trade is a 5% portfolio drawdown in a single session, not a recoverable paper loss.

- Trading 0DTE in low-VIX environments. When VIX is below 13, 0DTE ATM premiums compress to $2-3, bid-ask spreads remain $0.20-0.30, and the edge disappears into transaction costs. Wait for VIX above 15 or focus on longer-dated expirations.

- Ignoring gamma exposure concentration. On high-volume 0DTE days, gamma concentrates around round-number strikes (5100, 5150, 5200). Price gravitates toward or away from these strikes based on market maker hedging flows. Trade with awareness of where gamma is positioned, not against it.

Key Takeaways

- 0DTE options account for 59% of SPX options volume, making same-day volatility trading a structural market force rather than a niche strategy. The gamma effect from market maker hedging amplifies intraday moves.

- VIX1D (1-day implied volatility) trades at a 20-40% premium to VIX in calm markets and can spike to 2-3x VIX during stress. Use VIX1D, not VIX, to assess 0DTE option pricing conditions.

- Theta decay on 0DTE options follows an exponential curve: $0.15-0.25/hour at the open, $0.40-0.55/hour at midday, and $0.80-1.20/hour in the final hour. Structure trades around this decay timeline.

- Optimal 0DTE trading windows: 9:45-10:30 AM for directional trades, 10:30-11:30 AM for prime scalping, 11:30 AM-1:30 PM for premium selling. Avoid the final 90 minutes without advanced gamma flow analysis.

- Position sizing is the primary risk control: never risk more than 1% of account capital on a single 0DTE trade. The leverage that creates opportunity also creates rapid loss potential.

- The VIX1D/VIX ratio above 1.3 signals elevated short-term uncertainty; ratios below 1.1 favor premium-selling strategies. This ratio provides a leading indicator before SPX moves.

- Volatility Box hourly models provide statistically derived intraday ranges for strike selection and directional breakout evaluation, recalculating each hour to reflect the current volatility environment.

Trade 0DTE with Hourly Volatility Data

Volatility Box hourly models recalculate expected ranges and key levels at the top of each hour across 595 symbols. For 0DTE trading, these levels provide statistically derived strike selection boundaries and directional breakout triggers, updated as intraday volatility evolves.