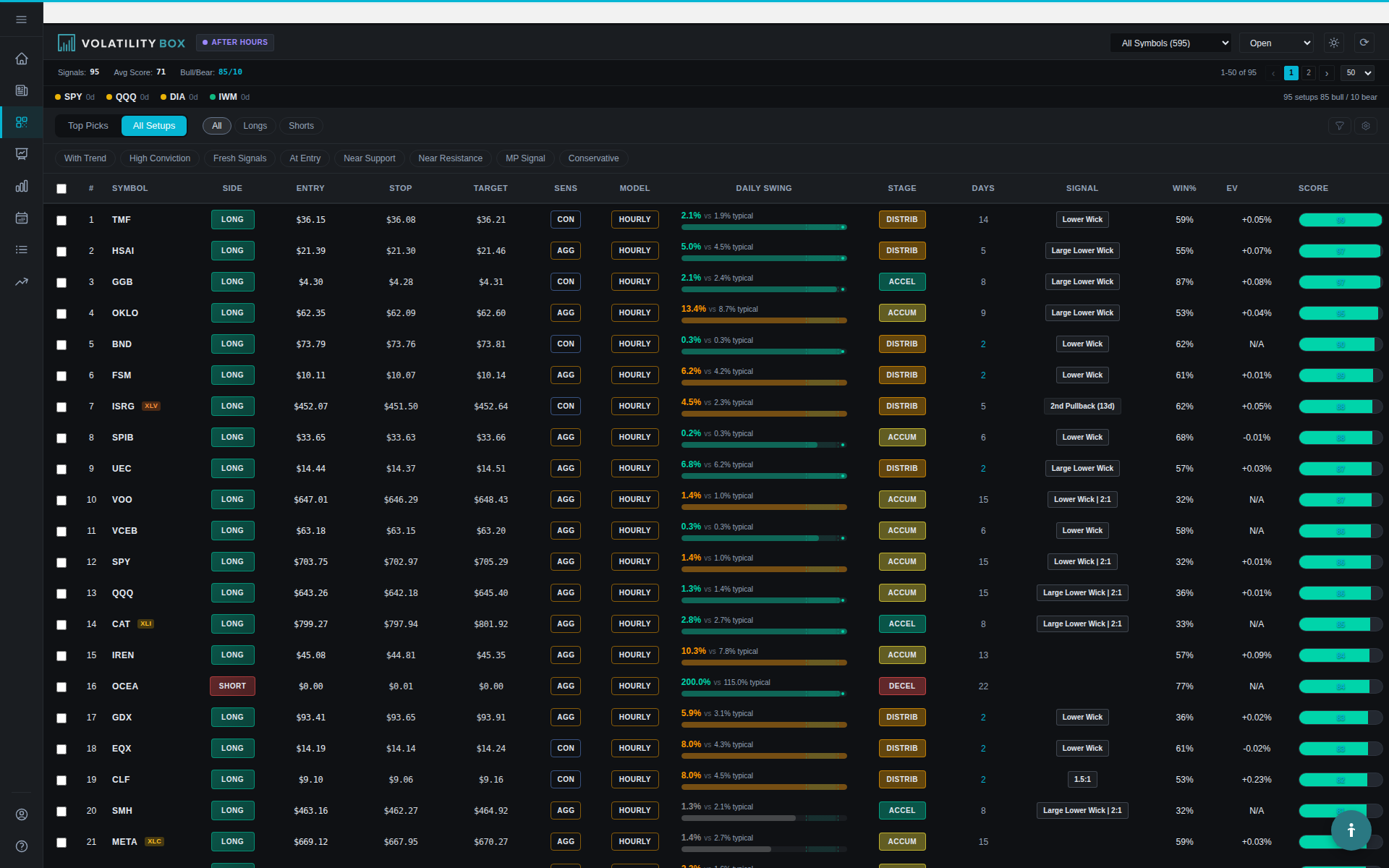

Pinpoint the intraday entry, level by level.

Hourly VB models mark the volatility levels where price is stretched right now, and they refresh through the session as conditions change. You act the moment a market lines up instead of an hour late.

Levels that move with the session.

Intraday volatility does not hold still, and neither do these levels. They mark where price is stretched as the day unfolds, so the entry you see is the entry that matters right now.

Marks the stretch

The levels show where price has pushed to an intraday extreme, the spot where a move is most likely to pause or turn.

Refreshes level by level

As the session moves through the hours, the levels update to match current conditions instead of leaving you with a stale morning read.

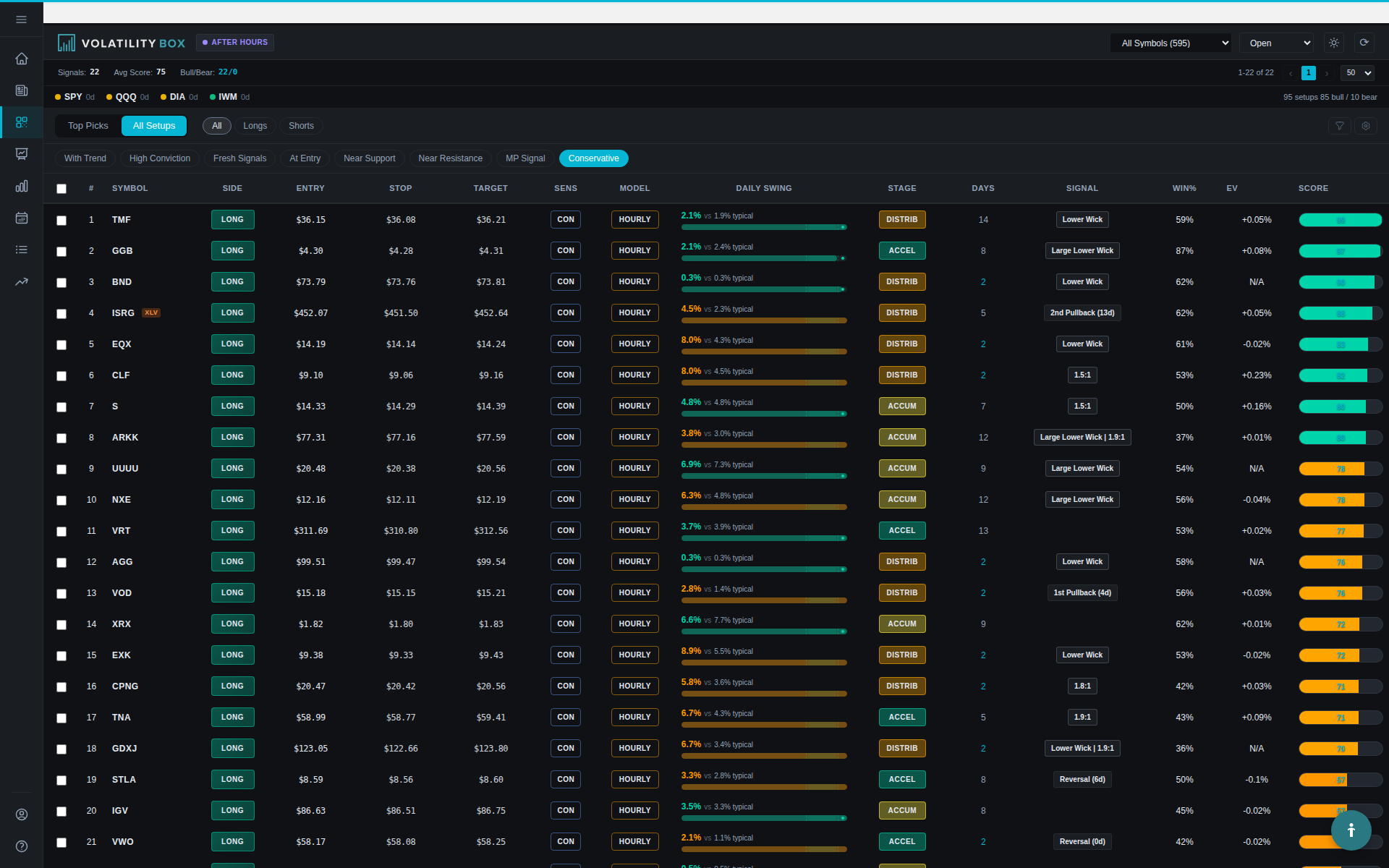

Conservative or aggressive

Choose the wider, more selective read or the tighter, more active one, depending on how many entries you want to work through a day.

Fresh entries all day

Because the levels keep pace with the session, missing one window does not end your day. The next refresh can hand you a new setup.

Conservative or aggressive, your call.

The conservative variant triggers at wider extremes. It hands you fewer setups, but each one marks a genuine intraday dislocation. It suits traders who want a small number of high quality entries per session.

The aggressive variant uses tighter levels and fires more often. Active day traders who want more chances to work lean on it as their primary read. Pick the one that fits how you trade, or watch both side by side.

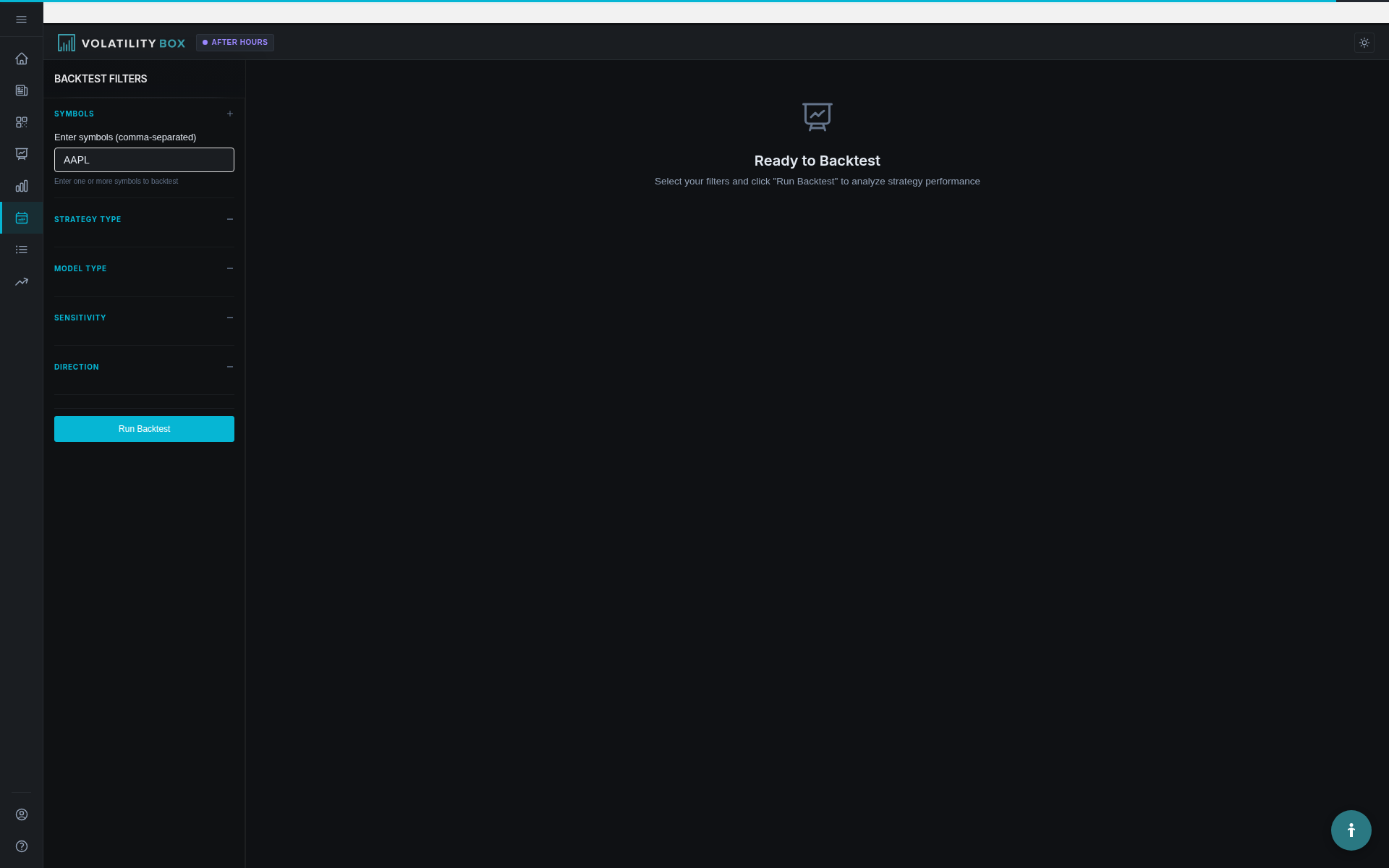

See how it held up, before you trust it.

You do not have to take the levels on faith. Validate them against history and see how the intraday read behaved across many past sessions, so you go in knowing what to expect.

- Test before you commit by reviewing how the levels played out across past sessions.

- Compare the variants so you can choose the conservative or aggressive read with eyes open.

- Trade with realistic expectations rather than hoping a fresh setup behaves the way you imagine.

An hour late is a different trade.

Intraday edges are gone almost as fast as they appear. Levels that refresh through the session keep you on the live read, so you enter while the move is still there instead of chasing it.

Act on the live read

The levels reflect where price is stretched now, not where it sat an hour ago. You decide on current conditions.

Pace yourself through the day

Fresh levels at each refresh mean more chances to enter, so one missed window does not cost you the whole session.

Pairs with the daily models

Hourly tells you where to enter. The daily models tell you whether the broader picture supports the trade. Together they give you two timeframes of context.

What traders say.

Catch the entry while it is still live.

Stop trading an hour behind the market. Let the levels keep pace with the session.